Q: Can the Premiums for Tokio Beyond Insurance Products Be Tax-Deductible?

A: The premiums for Tokio Beyond insurance products can be partially tax-deductible, specifically for costs related to the administration of the insurance, life insurance premiums, and management fees. However, the portion of premiums allocated to investment is not eligible for tax deduction under the insurance tax deduction category.

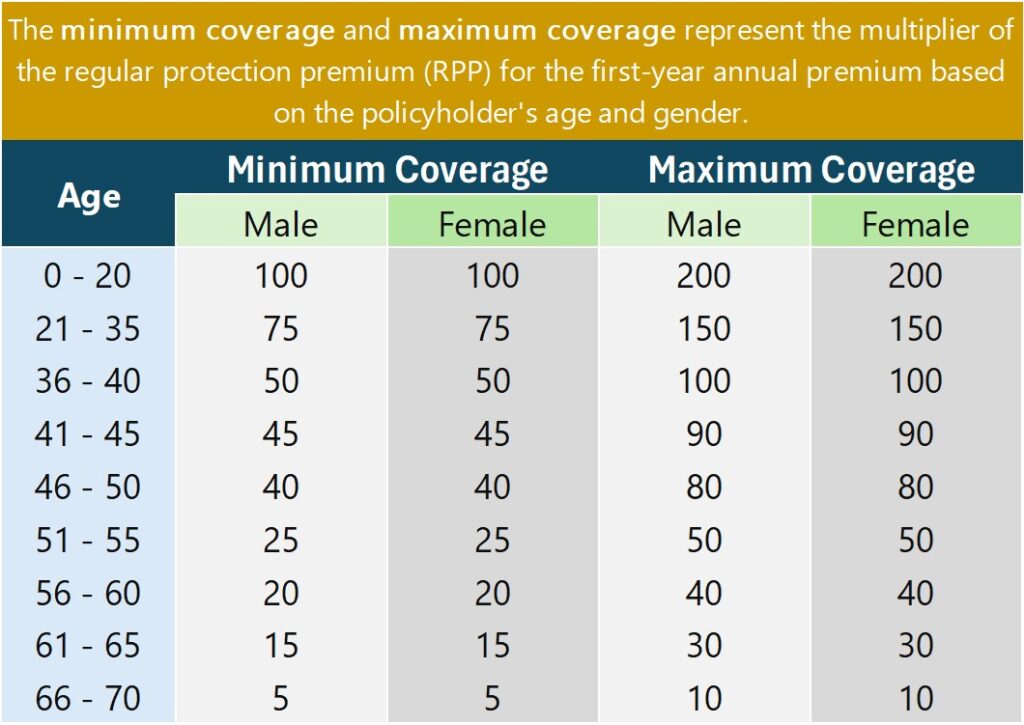

Q: What is the eligible age range for Tokio Beyond insurance?

A: The insurance policy is available for individuals aged 0 to 70 years, with coverage extending up to 99 years.

Q: What is the Sum Assured for Regular Protection Premium?

A: The sum assured for regular protection premium refers to the flexible life insurance coverage amount. Policyholders can specify their desired coverage amount, and the initial sum assured is calculated based on the premium paid for the regular protection premium per year.

Q: What is the Minimum Sum Assured for Regular Protection Premium?

A: Policyholders can determine the minimum sum assured based on the annual regular protection premium amount. The sum assured for the first year is equivalent to the annual premium amount, and it varies depending on the policyholder’s age and the terms and conditions set by the company.

Notes:

-

The sum assured for regular protection premiums after adjustments must not fall below 50% of the initial sum assured for the first-year regular protection premiums. On the effective date of the policy adjustment, the minimum sum assured will not be lower than the value calculated according to the company’s guidelines.

-

For policyholders aged 55 years or above, and whose annual premium payment exceeds 10 times the regular protection premium, the sum assured after adjustments can be reduced to a minimum of 5 times the annual regular protection premium.

Q: What is Non-Lapse Guaranteed Coverage?

A: Non-Lapse Guaranteed coverage is a benefit that ensures continuous life insurance protection for policyholders, provided they continue paying the required premiums for the regular protection coverage. This guarantee includes no reduction in the regular protection premium and no withdrawals from the redemption of investment units related to the premium for protection coverage. The company guarantees life coverage equivalent to or greater than the redemption value of the investment units.

Q: During the First 5 Years of Non-Lapse Guaranteed Coverage, Do Customers Need to Pay Regular Premiums Continuously?

A: Yes, customers must fulfill the following conditions:

- The policyholder must pay the regular protection premium in full as per the agreed payment schedule, without any interruptions.

- The policyholder must not withdraw funds from the redemption value of the investment units related to the regular protection premium.

- The redemption value of the investment units must be sufficient to cover all associated costs, including unpaid policy fees and other administrative fees (if applicable).

If these conditions are not met, the Non-Lapse Guarantee benefit will no longer apply.

Q: What is a Premium Holiday for Regular Protection Premiums?

A: A Premium Holiday for regular protection premiums refers to using the redemption value of investment units automatically to cover costs, ensuring continued insurance protection even when premiums are not actively paid. This continues until the redemption value is insufficient to cover the required costs. During the Premium Holiday period, the policy still provides life coverage for the policyholder.

Q: When Can a Premium Holiday for Regular Protection Premiums Be Used?

A: A Premium Holiday can be used after the policyholder has completed 2 years of premium payments and has sufficient redemption value in the investment units. These units will be automatically redeemed to cover the required costs, ensuring continuous coverage equivalent to the redemption value of the units. Redemption units must also cover policy administration fees.

Q: If a Policyholder Has Additional Riders and Wishes to Suspend Premium Payments for Regular Protection Coverage, What Happens?

A: In cases where the policyholder has additional riders attached to the policy and opts to suspend premium payments, the company will proceed by redeeming units from the investment value of the policy to cover the premiums for the regular protection coverage. This redemption will follow the standard policy process, deducting from the policyholder’s investment units to pay for the regular protection premium and any additional riders.

If the redemption value is insufficient to cover the premiums for the additional riders, the policyholder’s additional riders will terminate immediately once the premium payment period expires, and coverage will cease for those riders.

Q: Can funds be withdrawn from the Tokio Beyond policy in case of urgent financial need?

A: Yes, policyholders can withdraw a portion of the funds or redeem units from the investment value associated with the regular protection premium. This withdrawal is allowed to maintain coverage, and fees will be applied according to the terms and conditions of the policy.